Inflation began its ascent in 2021, largely fueled by pandemic-induced disruptions in the supply chain and the complexities of reopening economies. The situation escalated further with the onset of the Russia-Ukraine conflict in February 2022, which ignited a commodity super cycle—a broad and persistent surge in energy and raw material prices—resulting in inflationary shockwaves that reverberated through nearly all major economies. In the U.S., consumer price index (CPI) inflation reached a staggering peak of 9.1% in June 2022 (see Figure 1). However, the more intriguing aspect of this narrative is not how inflation surged but how it began to recede starting in 2023.

Figure 1. Core and Headline Inflation

Headline inflation surged in 2022 and then swiftly declined, while core inflation took a more leisurely descent.

Source: FRED and author’s own calculations

During the inflationary surge of 2022, many experts forecasted that a prolonged period of elevated unemployment would be necessary to bring inflation back down to the Federal Reserve’s target of 2%. This outlook paralleled the principles of the Phillips curve, which posits a trade-off between inflation and unemployment. The foundation of this belief rested on the sacrifice ratio, which quantifies the increase in unemployment typically needed to achieve a one percentage point reduction in inflation.

Historical trends indicated that this sacrifice ratio would be significant. Yet, to everyone’s surprise, inflation fell notably without a corresponding spike in unemployment, which hovered between 3.6% and 3.9% during 2021 and 2022. In fact, the sacrifice ratio appeared to be nearly nonexistent.

This raises a compelling question: did economists overestimate the durability of supply-side shocks and the relationship between inflation and unemployment? Evidence suggests that the Phillips curve may be flatter than previously thought, implying that inflation is less sensitive to fluctuations in unemployment. Furthermore, inflation expectations have been remarkably anchored around that 2% target (Blanchard and Bernanke, 2023).

Fast forward to the economic landscape of 2025–26, and we find ourselves in a markedly different—and perhaps more daunting—situation than what we encountered in 2022–23. Tariffs imposed during 2025–2026 provide crucial insights into how:

- 1. Supply-driven inflation operates, and

- 2. Policy can effectively combat inflation without necessitating sacrifices in employment.

The average U.S. tariff rates surged from 2.4% to nearly 18% in 2025, resulting in $195 billion in customs duties for fiscal year 2025 (Yale Budget Lab, 2025). Surveys indicate that American firms anticipate tariffs will account for 40% of their total unit cost growth during this period (Bostic, 2025). Concurrently, over 55% of businesses now regard geopolitical factors as a primary concern for supply chains, an increase from just 35% in 2023 (Risk Management Magazine, 2025).

The decline in inflation without a corresponding rise in unemployment underscores the necessity of considering supply-side dynamics and the anchoring of expectations in macroeconomic policy.

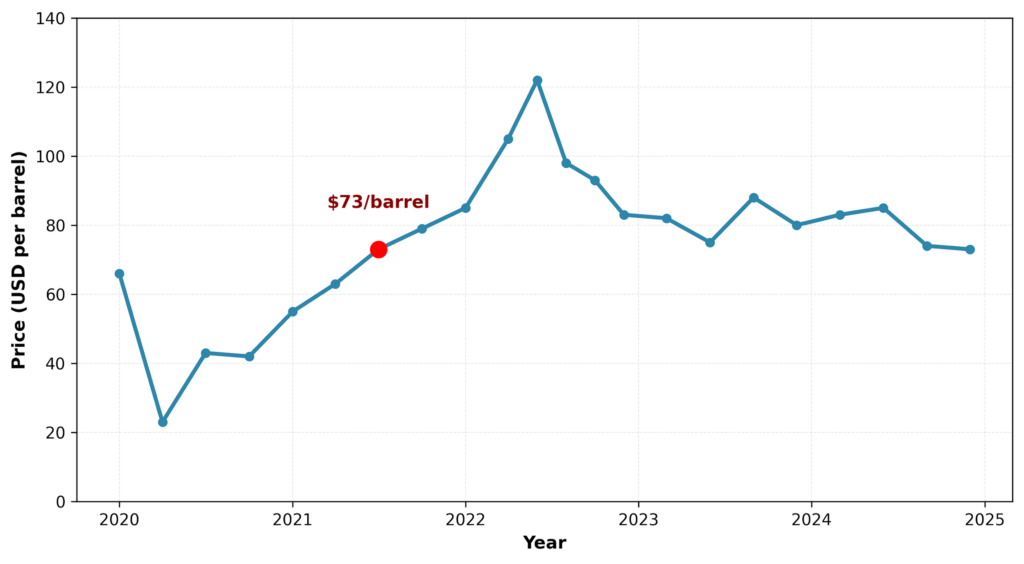

Interestingly, the supply chain disruptions and energy price shocks that plagued the 2022–23 inflationary period turned out to be less persistent than anticipated. Energy prices plummeted from over $120 per barrel in June 2022 to a range of $70–$90 per barrel by late 2023 (see Figure 2). Moreover, global supply chain pressures began to ease by mid-2023 (Morales, 2025). Economists miscalculated the duration of these shocks, erroneously believing that supply and energy pressures would linger well into 2024 rather than normalizing by mid-2023.

Figure 2. Brent Crude Price

Brent crude prices underwent a significant decline from their mid-2022 zenith to substantially lower levels by late 2023.

Source: FRED

Lessons from the inflationary experience of the 1970s suggested a prolonged supply-side shock with associated unemployment costs during disinflation (Dolan, 2023). However, the supply-side landscape of the 2020s presents distinct characteristics. Additionally, tariff-induced supply shocks operate differently than those stemming from pandemic-related disruptions.

Analysis by Cavallo, Llamas, and Vasquez (2025) reveals that prices for imported goods rose approximately 4%–6.2% between March and September 2025, while domestic goods experienced an increase of 2%–3.6%. The inflationary pressures from tariffs extend beyond just imported goods, as domestically produced items have also seen price hikes.

In a surprising turn, the labor market displayed resilience during this tumultuous period. Returning workers managed to keep wage growth moderate, despite low unemployment levels. Wage growth decelerated from 5.9% in March 2022 to 4.3% in October 2023, reflecting easing labor market pressures and a lower inflation rate without sacrificing employment (see Figure 3). Contrary to initial expectations, the influx of available workers allowed firms to hire without significantly increasing wages, resulting in a deceleration of pay growth, even with unemployment remaining low.

Figure 3. Wage Growth and Unemployment Rates in the US

Wage growth slowed even as unemployment remained low.

Source: FRED and author’s own calculations

The Federal Reserve’s credibility played a pivotal role in anchoring inflation expectations around its 2% target. When such expectations are “anchored,” the public tends to trust that inflation will remain close to 2%, mitigating the likelihood of planning for significant, ongoing price increases. The Fed’s credibility, combined with a proactive communication strategy, has seemingly fostered an environment that mitigated second-round effects from wage-price spirals (where rising wages lead to increased costs, which then drive further price hikes). This marks a crucial shift in policy from adaptive to anchored expectations aligned with the central bank’s stated goals.

Before the inflationary turmoil of 2021–2022, the concept of an inflation-targeting central bank and the anchoring of inflation expectations were largely theoretical. This dynamic was vividly illustrated as unemployment remained historically low while inflation gradually subsided, as evidenced by the five-year breakeven inflation rates that stabilized around 2%.

Despite the looming tariff pressures, long-term inflation expectations have remained relatively stable. In November 2025, Atlanta Fed President Raphael Bostic asserted that inflation poses a significant risk to the Fed’s dual mandate of ensuring price stability and maximum employment, while Fed Vice Chair Philip Jefferson remarked that the “lack of progress” on the inflation target “appears to be due to tariff effects.” The challenge confronting policymakers lies in distinguishing between one-time price level impacts from tariffs and persistent inflationary pressures that necessitate monetary tightening (raising interest rates to temper demand).

The inflationary episode from 2021 to 2023 illustrates that supply-driven disinflation can occur with a nearly zero sacrifice ratio when shocks are temporary and expectations remain anchored. Yet, the landscape of 2026 presents a different set of challenges. Inflation continues to exceed the Fed’s 2% target, and the labor market is displaying signs of weakness. With unemployment on the rise, the Fed cannot simply replicate the 2021–2023 strategy of waiting for supply pressures to dissipate while maintaining a tight policy stance. Any further monetary tightening in response to tariff-induced inflation risks exacerbating job losses, hampering hiring, and stunting income growth for workers.

A critical takeaway for policymakers is to avoid neglecting supply-side dynamics—such as disrupted supply chains or sudden surges in raw material costs that drive prices upward from the production side. They must factor in the transient nature of supply shocks in future inflation projections. This lesson is particularly relevant to the current context of tariff-induced inflation. While the Federal Reserve can uphold expectations anchoring through clear communication, it cannot counteract the direct price level implications of tariffs without incurring economic costs. The challenge is further complicated by the fact that tariffs are discretionary policy decisions rather than exogenous shocks.

The experiences from 2021 to 2023 and the evolving scenario in 2025–2026 underscore the necessity for coordination between monetary and trade policy. Recent analysis by Yahoo Finance (2025), informed by J.P. Morgan Global Research, estimates that the announced tariff measures could inflate Personal Consumption Expenditures prices by 1.0–1.5 percentage points in 2025. Maintaining the credibility of the central bank is paramount, as it risks erosion if policy-driven shocks repeatedly push inflation above target.

The conundrum in 2025–26 revolves around addressing a different breed of supply shock, one driven by trade policy distortions rather than traditional supply-chain disruptions, yet with minimal economic upheaval.

Ultimately, the key lesson for policymakers is that when inflation expectations are anchored and supply shocks are clearly delineated from demand pressures, the costs associated with disinflation can be significantly lower than conventional models suggest. Achieving disinflation at such low costs demands both policy coordination and sustained central bank credibility in an unusually unpredictable environment.

Stock Dropped 50%")