[ Note: This article was originally published on March 10, 2025 by Scott Sumner at his substack under the title “False Dawn: George Selgin on the New Deal.”]

- A Book Review of False Dawn: The New Deal and the Promise of Recovery: 1933-1947, by George Selgin.

Franklin Delano Roosevelt’s New Deal initiatives aimed to achieve three crucial objectives: recovery, relief, and reform. In his insightful book, George Selgin scrutinizes the first goal—recovery. Did the New Deal effectively lift the United States from the depths of the Great Depression?

The brief answer is a resounding no. However, False Dawn: The New Deal and the Promise of Recovery 1933-1947 is not simply an anti-Roosevelt diatribe. Selgin presents Roosevelt’s policies as a mixed blessing; while some aspects indeed fostered recovery, others were counterproductive, stifling economic progress. Consequently, the U.S. economy remained stagnant well into 1940, even as global tensions escalated with the onset of the European War.

My research throughout my career has largely concentrated on two pivotal factors: the global gold market’s influence on aggregate demand and the repercussions of Roosevelt’s high-wage policies on aggregate supply. Yet, Selgin casts a broader net, examining a diverse array of New Deal policies, and I anticipate this accessible book will become the definitive reference on the macroeconomic ramifications of the New Deal.

I will begin by analyzing the New Deal’s influence on aggregate demand before moving on to its effects on aggregate supply. Finally, I will conclude with reasons why Selgin’s book deserves your attention.

1. The New Deal and Aggregate Demand

Roosevelt had two primary macroeconomic aims. During his campaign, he promised to reflate the price level back to its 1926 status and boost employment and production from the dismal levels of early 1933. Ironically, FDR was skeptical about the two policy tools now deemed essential by macroeconomists: fiscal stimulus and money printing.

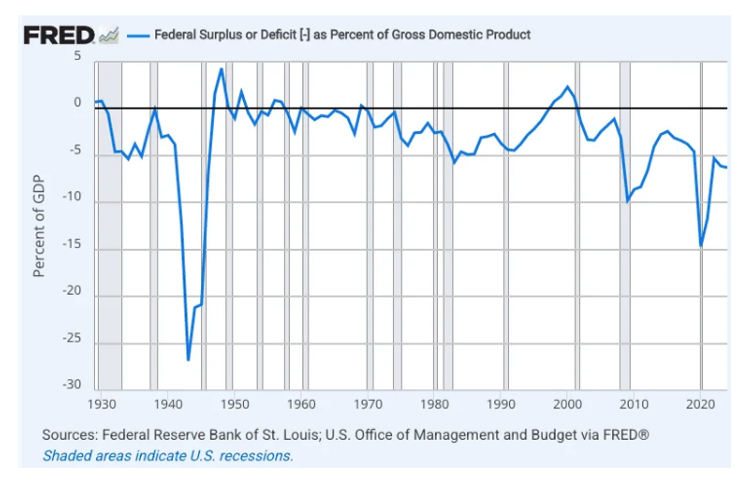

Figure 1 illustrates the federal budget deficit as a percentage of GDP:

Note how the budget shifted from a surplus in 1929 to a deficit around 5% of GDP under President Hoover, before remaining relatively stable until World War II. Contrary to popular belief, Hoover was an active president, implementing discretionary fiscal stimulus at a time when federal spending was just 3% of GDP—hardly a beacon of government intervention.

Many economists recognize that FDR campaigned on a promise of fiscal prudence yet ended up running deficits. They might assume he was a hidden Keynesian, leveraging fiscal stimulus as part of the New Deal. Selgin debunks this myth; FDR was genuinely opposed to peacetime deficit spending and didn’t ramp up the budget deficit until WWII. Any success of the New Deal cannot be attributed to fiscal stimulus.

A more compelling case can be made for FDR’s monetary policies, albeit not in a contemporary sense. The improvement in monetary conditions stemmed primarily from three key factors:

- a. A stabilized banking system

- b. Dollar devaluation

- c. Gold inflows from Europe

Taking office on March 4, 1933, during a severe banking crisis, Selgin reveals that major New York banks were sound, but the Federal Reserve banks faced insolvency as skittish investors converted currency to gold, fearing dollar devaluation. Before his inauguration, FDR had hesitated to commit to a gold standard.

There was a four-month interregnum between the election and inauguration, during which both Hoover and FDR share partial blame for letting conditions deteriorate. Ironically, this chaos provided FDR with a unique opportunity to implement radical reforms once he took office.

Unfortunately, Roosevelt lacked a coherent understanding of which experiments would yield the best results. The initial bank holiday leaned heavily on ideas from banking experts who had been attempting to formulate similar plans during Hoover’s final days. FDR’s resistance to federal deposit insurance was ultimately overridden by Congress, who insisted on including it in a broader banking reform package—perhaps correctly fearing it would encourage reckless banking behavior.

Raising the dollar price of gold from $20.67/ounce to $35/ounce did indeed provide a significant stimulus to the economy. However, this boost would have been even more pronounced had the increase been monetized—something FDR opposed, as it smacked of “printing money.” Consequently, the economy had to depend on increased money velocity during the early recovery stages, which fortunately improved due to a more stable banking system and inflation expectations stimulated by dollar devaluation.

Throughout the mid to late-1930s, additional monetary stimulus materialized from gold inflows from Europe, enhancing the monetary base. However, these gold inflows were more a consequence of external pressures than New Deal policies, reflecting the U.S. economy’s advantage amid rising European war fears.

Selgin regards FDR’s dollar devaluation as an overall positive for economic recovery, albeit with some reservations regarding its execution. Most economists concur with Keynes’s quip that George Warren’s gold-buying program of late 1933 resembled a “gold standard on the booze,” with daily adjustments to the federal gold buying price. While I remain one of the few economists defending this program, the nuances are minor compared to Selgin’s broader evaluation. FDR managed to reverse the economic contraction and elevate nominal spending through banking stabilization and dollar devaluation, but he squandered opportunities for a faster recovery by neglecting standard monetary and fiscal policy tools.

In the end, FDR failed to achieve his 1926 price level target; indeed, the price level remained below pre-Depression levels until WWII. Nevertheless, the uplift in aggregate demand should have prompted a satisfactory recovery, had it not been hampered by other detrimental factors. A comparable nominal GDP growth following the 1920-21 depression resulted in a swift recovery. Instead, the economy of the 1930s languished due to counterproductive supply-side policies, which I will explore in the next section.

2. The New Deal and Aggregate Supply

My research on the Depression has typically emphasized FDR’s high-wage policies. However, Selgin highlights that these wage initiatives were merely one facet of a much broader effort to construct private sector cartels. The Agricultural Adjustment Act (AAA) sought to curb farm output and elevate prices, while the National Industrial Recovery Act (NIRA) aimed for similar outcomes across other sectors.

These programs epitomize the fallacy of reasoning from a price change. While depressions triggered by inadequate aggregate demand often coincide with falling prices, it does not follow that raising prices through supply restrictions will spark an economic boom. It’s akin to claiming that because Rolls Royce owners are typically wealthy, purchasing a Rolls Royce is a surefire path to riches.

The AAA and NIRA employed a mix of incentives and penalties to persuade farmers to curtail output and raise prices, while manufacturers were urged to decrease output and hours worked while simultaneously boosting hourly wages. Today, the notion that the Great Depression stemmed from overproduction leading to price drops seems ludicrous, yet this type of reasoning from price changes can lead one to the absurd conclusion that producing less could remedy a depressed economy!

Few economists have been as vocal as George Selgin in warning against the dangers of flawed reasoning based on price changes. His book Less Than Zero provides an excellent examination of the pitfalls associated with price level targeting and advocates for a more effective NGDP targeting approach. Surprisingly, some contemporary economists argue that NIRA may have had a stimulating effect by raising inflation expectations; however, higher inflation is only beneficial when resulting from increased aggregate demand—not diminished aggregate supply.

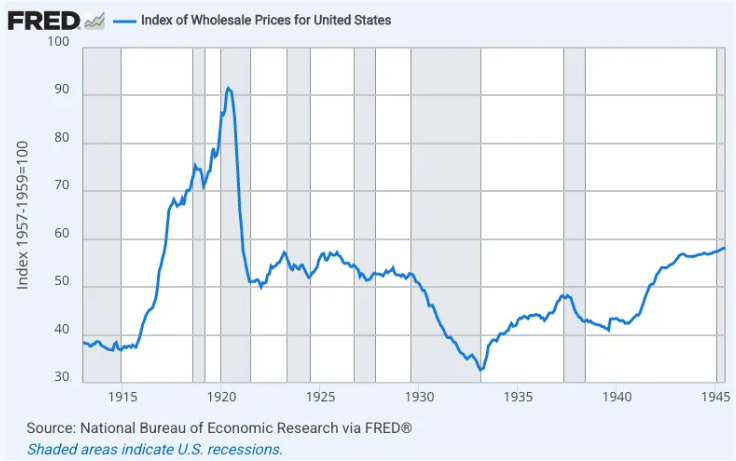

Selgin underscores the adverse effects of cartelization policies like the AAA and NIRA, which were likely the most significant obstacles to recovery. In percentage terms, prices rebounded more quickly after the 1929-33 downturn than following the 1920-21 contraction, as illustrated in Figure 2.

However, the output recovery post-1921 was substantially more robust. The post-1933 increases in both wholesale prices and NGDP should have facilitated a satisfactory recovery, had it not been interrupted by adverse supply conditions like the AAA and NIRA.

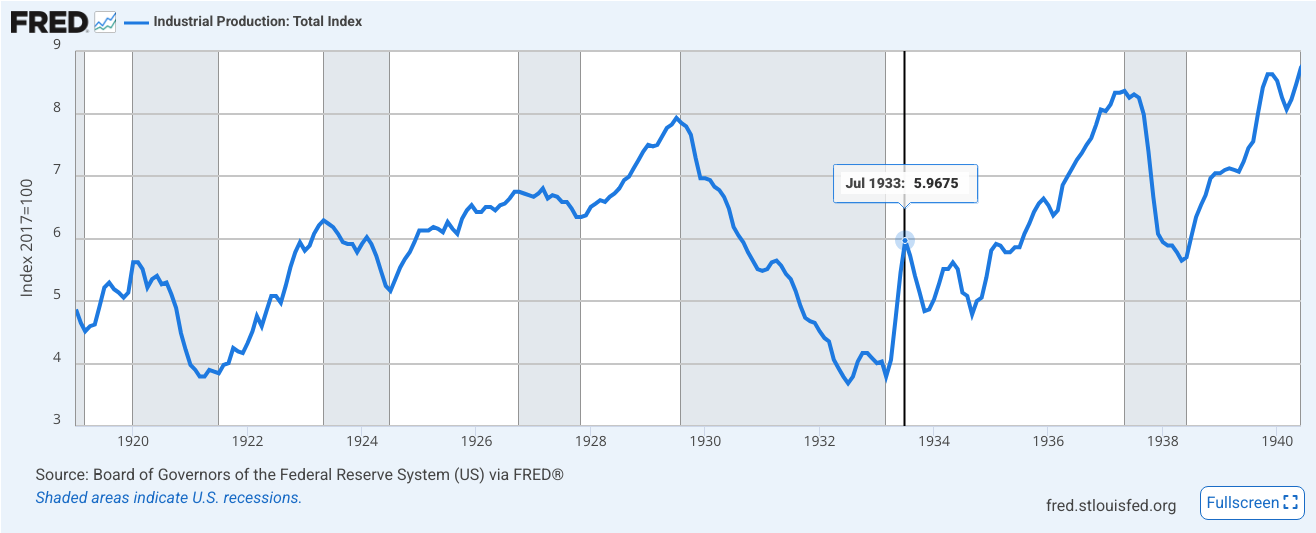

Figure 3 shows how industrial production stagnated for two years following the announcement of the President’s Reemployment Agreement in late July 1933. The NIRA’s policy of raising nominal wages by approximately 20% within two months stifled a promising recovery already initiated by dollar devaluation. Following the NIRA’s unconstitutionality ruling in May 1935, a vigorous recovery resumed, only to be thwarted again by another wage shock in late 1936 and 1937, partly fueled by aggressive unionization efforts supported by the Wagner Act.

The 1937-38 depression marked a significant setback for FDR. Alongside the wage shock, Selgin points out various policies that hindered business growth, including the newly implemented undistributed profits tax, which dissuaded firms from utilizing retained earnings for investment projects. The administration’s rhetoric, which claimed a capital strike by economic elites was responsible for the depression, did little to alleviate concerns.

Aggregate demand dipped in late 1937, fueled by measures such as gold sterilization and increased reserve requirements. Despite prices remaining well below pre-Depression levels, the price hikes of 1936-37 incited fears of speculative excess that could trigger another 1929-like crash. FDR’s desire for prices to revert to 1926 levels without any inflation was a tall order.

Keynesians often attribute the 1937 slump to fiscal austerity, yet evidence suggests that the fiscal contraction was insufficient to account for one of the 20th century’s most severe recessions. In fact, a similar austerity approach in 2013 did not result in any economic slowdown, despite occurring during a zero lower bound period where fiscal austerity is expected to be particularly detrimental. Much of the 1937 “austerity” stemmed from the fact that a one-time veteran’s bonus payment in 1936 was not repeated the following year.

Selgin’s exploration of the unexpected postwar prosperity is particularly insightful, as it counters the Keynesian prediction of a post-war depression following drastic cuts in military expenditure. Instead, the economy thrived, a shift Selgin attributes to the transition from New Deal regulatory policies to more market-friendly, pro-business strategies.

3. Why You Should Take This Book Seriously

Selgin’s book is compelling, but will mainstream economists be willing to entertain it? FDR is often regarded as a liberal icon and one of the most significant presidents in U.S. history. Historically, critiques of FDR’s legacy have often come from the fringes. While Selgin does not adhere to rigid ideological boundaries, his moderate libertarian perspective could make some center-left economists hesitant. So, why should they take this book seriously?

First, it’s important to note that John Maynard Keynes emerges as a central figure in this narrative. Selgin’s assessment of the New Deal resonates with Keynesian principles. Keynes would have likely preferred FDR to utilize conventional fiscal and monetary stimulus while avoiding radical cartelization policies and anti-business rhetoric that stifled business confidence.

Second, Selgin does not dismiss all of FDR’s recovery measures; he concedes that banking reforms and dollar devaluation contributed positively to aggregate demand.

Third, Selgin emphasizes that his somewhat skeptical view of the New Deal’s recovery efforts does not equate to a blanket condemnation of the program itself, which also encompassed relief and reform. A progressive could reasonably argue that the New Deal was beneficial overall, thanks to enduring reforms like the Social Security Act and the SEC, along with various relief measures for the unemployed, despite its shortcomings in fostering robust recovery in production and employment.

“If FDR’s New Deal was effective, why wasn’t it repeated in 2009?”

It’s worth pondering why, during the relatively mild Great Recession of 2008-09, which bore similarities to the Great Depression, neither Democratic leaders nor center-left economists showed much interest in resurrecting a New Deal. Rather than pursuing cartelization, they opted for policies that FDR would have likely rejected, such as fiscal stimulus and the controversial practice of Quantitative Easing. If FDR’s New Deal truly worked, why was it not replicated in 2009?

This book transcends the polemic some center-left readers might expect. It’s entirely plausible to view FDR as a liberal champion who helped win WWII, thwarted fascism, and fostered a more compassionate society through social insurance programs, while still critiquing the New Deal’s effectiveness in stimulating recovery. After all, many developed nations rebounded more swiftly than the United States, with the notable exception of France, which had its own dysfunctional NIRA-like framework.

In the past, some progressives were critical of James Hamilton for asserting that New Deal initiatives like the AAA and NIRA were counterproductive. His response to the backlash was succinct:

- “I openly confess to believing that government policies that were explicitly designed to limit manufacturing, agricultural, and mining output may indeed have had the effect of limiting manufacturing, agricultural, and mining output.”

For more on these topics, see

In light of recent electoral challenges, many progressive thinkers are reevaluating public policy. While they continue to advocate for social insurance, some center-left commentators are increasingly highlighting the need for policies that promote greater “abundance,” which necessitates a focus on supply-side reforms. I strongly encourage these commentators to engage with Selgin’s work, which offers valuable insights relevant to today’s economic landscape.

*Scott Sumner is Professor Emeritus in Economics at Bentley University in Waltham, Massachusetts, and a Research Associate on monetary policy at the Mercatus Center. He earned his Ph.D. in economics at the University of Chicago in 1985. He blogs both at EconLog and also at his personal blog at substack, The Pursuit of Happiness.

As an Amazon Associate, Econlib earns from qualifying purchases.