The widespread misconception that drivers finance roads primarily through gas taxes and tolls significantly influences discussions about transportation funding. This misconception not only affects the discourse on how transportation is funded but also shapes perceptions of the transportation system itself.

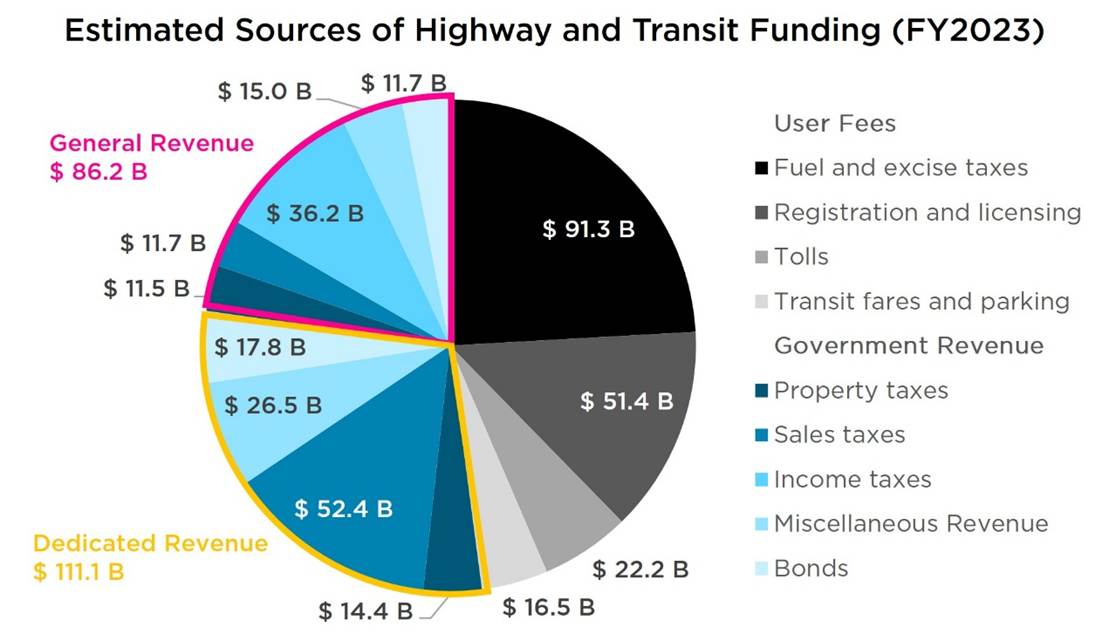

Historically, the United States has relied on various local, state, and federal taxes and fees to fund its transportation infrastructure. These funding sources can be categorized into three main types: 1) general government taxes, such as property, sales, and income taxes; 2) user fees, which include charges like tolls and fuel taxes levied on transportation system users; and 3) Pigouvian taxes, which address external harms, including congestion fees and carbon taxes.

The combination and design of these revenue sources influence perceptions of the transportation system, determining who pays, why, and how much. These factors also dictate whose interests are considered in transportation decision-making, who benefits, and who bears the system’s costs. This article explores various funding mechanisms and how each can contribute to creating a more equitable transportation system.

How funding sources contribute to transportation equity

Each funding source discussed below involves specific choices, including the rate assessed and the entities to which it applies. These choices influence the relative burden on individuals and businesses accessing transportation services, impacting the system’s equity.

User fees, although not the primary revenue source for transportation, are commonly associated with transportation funding. While some registration fees may be linked to vehicle value, suggesting potential tax progressivity, user fees are generally regressive. For instance, lower-income households spend a larger portion of their income on transportation, particularly fuel, resulting in a disproportionate contribution to fuel tax revenue. Additionally, private drivers, regardless of income, effectively subsidize commercial trucking as commercial vehicles do not pay an equitable share for road use.

Currently, general funding from local, state, and federal governments accounts for approximately 23 percent of total transportation revenue. Additionally, another 29 percent comes from directed tax revenues, including property and sales taxes. Given the shared interest in transportation, broad public investment aligns with the government’s role in shaping transportation choices. The progressivity of this funding source increases when derived from income taxes. However, the recent shift towards sales taxes as a significant revenue source heightens the regressivity of government revenues, potentially adding to the disproportionate burden on lower-income families.

Pigouvian taxes can influence behavior, as demonstrated in New York City, where congestion pricing is used to reduce emissions and finance essential transit upgrades. However, these taxes can resemble user fees and may require complementary policies, like NYC’s low-income discount, to avoid penalizing individuals with limited transportation options.

Efforts to create a more sustainable and equitable transportation system must include discussions on how the system is funded, focusing on equity.

Property taxes

In the early days of the United States, local governments maintained roads, with property owners contributing fees or labor. Today, property taxes account for just 15 percent of local government contributions to transportation and less than 4 percent of total surface transportation revenue, primarily funding maintenance and operations. When considering general government fund transfers, property taxes likely represent around 7 percent of transportation funding, a significant decrease from their historical role.

👍Taxing land value generates revenue from those who financially benefit from local transportation infrastructure.

👎Delays in property value increases due to improvements can hinder transportation development. Property taxes are often seen as regressive due to inaccurate assessments, but local policy nuances significantly affect the relative regressivity of specific property tax systems. Housing restrictions can create disparities in access to basic services, as seen during “white flight” to suburbs or through modern NIMBYism.

Tolls

As the nation grew, roads became vital for connecting cities, straining local resources and pushing state governments to facilitate travel. States, financially constrained after the American Revolution, turned to private entities to build and maintain roads. From turnpikes, named for the pike blocking travel until the fee was paid, to modern toll roads, this system requires users to pay directly for road use.

Today, tolls are often adjusted based on vehicle class, allowing additional funding from commercial vehicles due to their impact on infrastructure. However, tolls do not cover all costs related to vehicle traffic, such as congestion and pollution. Currently, tolls account for just 6 percent of transportation funding.

👍Directly charging users for road usage establishes a clear relationship between service provision and cost, similar to other public services like water and electricity.

👎Tolls create a system that favors higher-income households and can limit mobility for lower-income households. Tolls often focus solely on specific infrastructure rather than considering the entire transportation system.

Registration fees

In the early 20th century, motor vehicles became more common in the United States. New York was the first state to mandate vehicle licensing in 1901. With increasing vehicle numbers, states began collecting fees for vehicle registration and licensing, generating revenue to support road expansion. Today, registration and licensing fees contribute about 13 percent of transportation spending.

👍Vehicle registration and licensing serve safety-related purposes.

👎Similar to tolls, registration and licensing require upfront financial costs to participate in the car-dependent system. While some fees may be reduced for lower-income households, most states use a flat fee system, making them regressive. Furthermore, enforcement of these fees can perpetuate systemic racial bias through pretextual stops, biased penalties, and predatory fees.

Fuel taxes

Oregon implemented the first state fuel tax in 1919 to fund roads. Within a decade, fuel taxes became the primary fee collected from drivers. The federal fuel tax, introduced in 1932, was dedicated to transportation funding with the Highway Trust Fund’s creation in 1956. Throughout the 20th century, highway expansion was largely funded by fuel taxes, which now account for about 24 percent of road spending.

Some fuel taxes are allocated to general spending, though this amount is smaller than government funding for highways. A portion of state and federal fuel taxes supports public transit services, covering over 20 percent of transit expenditures nationwide.

👍Fuel taxes align with service usage, acting as a small incentive to improve vehicle efficiency and a disincentive against driving.

👎Fuel taxes are set independently of oil costs and highway usage. While historically used as a government revenue source, the link between fuel taxes and road use has been used to oppose non-highway transportation spending. Lower-income households spend a larger share of their income on fuel, making fuel taxes regressive.

Sales taxes

With unchanged federal fuel taxes for over three decades and a reduced share of transportation funding from vehicle and fuel taxes, many states and localities have turned to sales taxes to bridge the funding gap, dedicating sales tax revenue to state and local transportation funds or specific projects. In 1998, sales tax revenue accounted for 6 percent of all dedicated transportation funding; 25 years later, it comprised 14 percent. Including contributions from general government spending, sales taxes likely represent at least 17 percent of transportation revenue.

👍Sales taxes are mode-neutral and raise revenue from participants in the local economy, inherently linked to the local transportation system.

👎Sales taxes are even more regressive than fuel taxes and are unrelated to transportation use or need.

Congestion pricing

Recently, there has been increased focus on how price signals through taxes and fees can influence transportation system usage. New York City’s successful congestion fee program exemplifies this approach.

Every vehicle on the road adds to traffic, and each additional car or truck can slow down the system, increasing travel time for others. Congestion pricing is designed to encourage drivers to travel at off-peak times or seek alternatives.

There are various ways to design a congestion fee, but the key is tying it to traffic flow, whether by time (e.g., peak vs. off-peak hours), current traffic conditions (e.g., dynamic toll pricing), or zone (e.g., fees for entering congested city areas).

Since congestion pricing is a form of tolling, it shares concerns about regressivity and pay-to-play dynamics. However, income-related exceptions, like those in NYC’s program, can help address these issues. Additionally, directly linking congestion pricing revenue to support for alternatives can facilitate a shift towards less harmful, more equitable options like transit.

👍Congestion pricing helps internalize the implicit subsidies provided to drivers, ensuring they pay the true costs of driving. Congestion pricing revenue is often used to fund alternatives, expanding mobility options and reducing the adverse impacts of high-traffic areas.

👎Congestion pricing raises similar concerns as general tolling, potentially being regressive without countermeasures.

Carbon taxes

Another unaddressed cost of the auto-centric transportation system is vehicle emissions. All vehicles produce pollution through tire and brake wear, and combustion vehicles contribute tailpipe emissions, causing health issues for communities near roadways. Additionally, transportation is the largest source of heat-trapping emissions in the United States.

The transportation system’s reliance on fossil fuels stems from the lack of pricing for pollution-related harms. Drivers pay for gas but not for the health costs of particulate matter from tailpipes or for increased wildfire risks and other climate-related disasters from burning billions of gallons of gasoline annually.

Pigouvian taxes aim to internalize costs ignored by the market. Carbon taxes propose shifting climate change costs back to the pollution source. In transportation, this means adding the monetized climate harms of gasoline combustion to the gas price, encouraging efficient use and alternative solutions.

👍Carbon taxes help internalize the implicit subsidies provided to drivers, ensuring they pay for the climate costs of driving.

👎Systemic factors drive fossil fuel dependence, making carbon taxes potentially regressive for households without alternatives. Mitigating this impact could involve economic rebates or linking revenue to sustainable alternatives. Carbon taxes only address one form of vehicle pollution; additional policies are needed to address all harms.

Mileage-based fees / road user charges

Fuel taxes are an indirect road use fee—more efficient vehicles use less fuel for the same distance as less efficient ones, but both cause similar wear and tear within the same class. Directly charging users through a mileage-based fee, also known as road user charges (RUCs) or a vehicle-miles traveled (VMT) fee, could more accurately allocate infrastructure costs.

Some RUCs may be weight-based, better reflecting the trucking industry’s impact on roads. While no federal RUC exists, the Department of Transportation has funded state pilot programs.

👍Road user charges provide a clearer link between funding and use than fuel taxes. Shifting from a fuel tax to a RUC can be progressive, as higher-income households tend to travel more and own more efficient vehicles.

👎Low-income households spend a higher percentage on goods than services, and RUCs targeting commercial trucks can be more regressive than general sales taxes.

Personal and corporate income taxes

General government funding is the largest source of transportation funding today, and for most states and the federal government, personal and corporate income taxes are the main revenue sources for this spending.

👍Income taxes are generally progressive, with rates increasing for higher income levels.

👎Exemptions for capital gains and business income/losses can significantly reduce tax rates for wealthier households, flattening the overall tax code.

It’s not just about where the money comes from, but where it goes

There are numerous ways government and transportation agencies fund services, but the system is ultimately defined by how that revenue is spent. Although most revenue sources are regressive, progressive distribution prioritizing lower-income households’ mobility can lead to a more equitable transportation system.

Some funding mechanisms send signals to encourage sustainable choices, but choices are limited without viable alternatives. Many Americans face either costly car dependence or underfunded transit options with long wait times and limited access to jobs and essential destinations.

The latest forecasts from the Congressional Budget Office reveal a mismatch between federal revenue and spending, with the system likely to collapse by 2028. The root cause of the Highway Trust Fund’s potential insolvency is not the lack of fuel tax increases, but the failure to support diverse mobility options.

Whether through more equitable driver charges or increased Treasury funding, the next surface transportation bill must invest in a comprehensive, diverse transportation system to ensure Americans have the freedom to move.